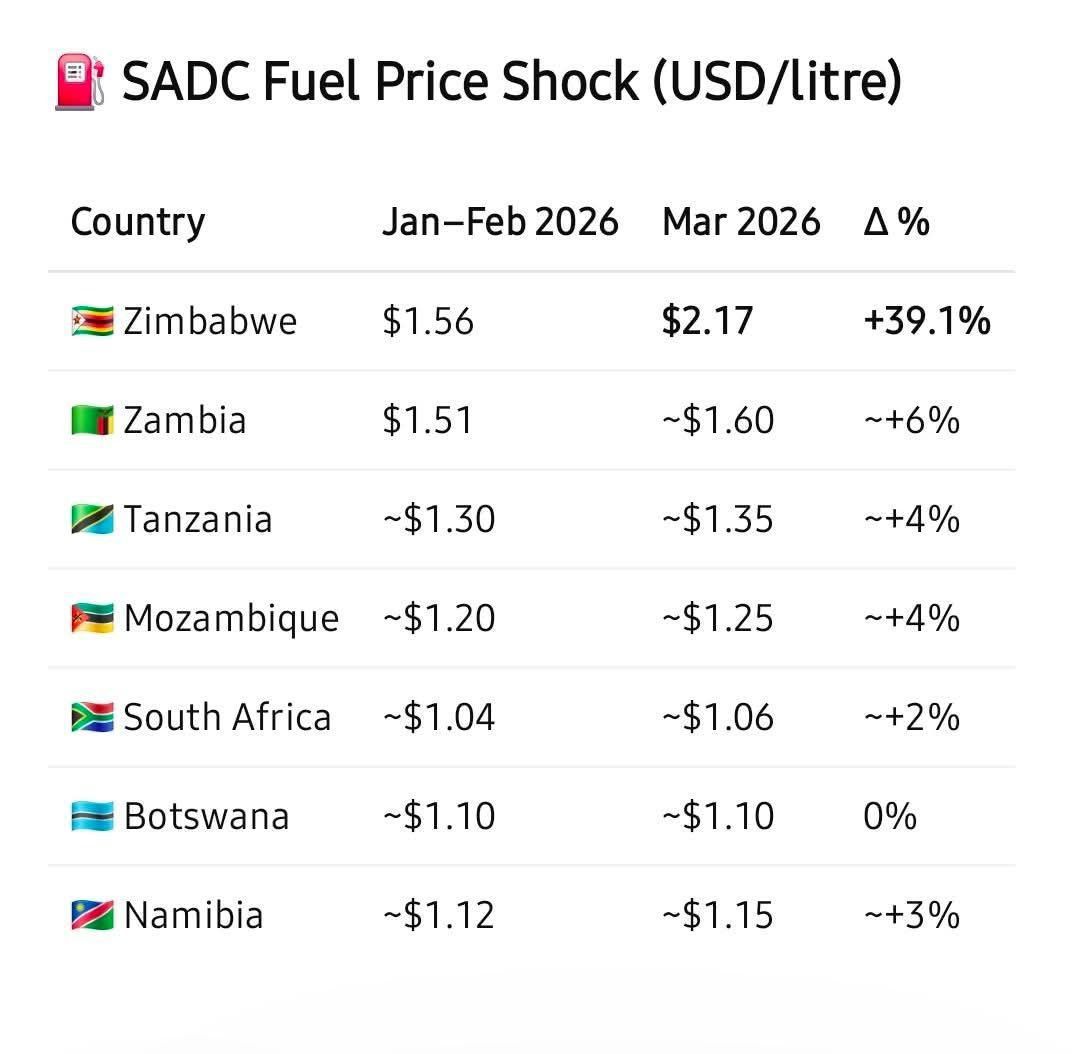

A LOT has been said about the price of fuel in Zimbabwe relative to other countries in the region in the wake of the Iran war and disruption to international fuel supply chains. But let us at least compare like with like.

It is pointless lining up pump prices in coastal economies with port access against those of landlocked countries that must drag fuel inland at great cost. The only sensible comparisons are Zambia and Botswana. And even there, Zimbabwe has moved first. The others will move too. They always do. The only real comparison is after everyone has had their turn at the pump.

That said, there are real issues here and they expose the structural deficits in the Zimbabwean economy. As some of us have argued for a while, there is a latent United States dollar inflation in Zimbabwe over and above the inflation of the greenback itself. The “base effect” crowd say otherwise, but that collapses under the lightest inspection.

Take a simple metric: US dollar interest rates in Zimbabwe are around 18 percent on the dollar. In neighbouring countries, including those with weaker currencies, comparable inflation dynamics are nowhere near as punishing. Fuel imports into Zimbabwe are financed through letters of credit carrying steep financing costs for local firms. That is not the prevailing reality in SADC comparables.

It is also worth considering that Zimbabwe may not have the reserves it says it has. If reserves were genuinely comfortable, the average cost of fuel would cushion short-term spikes in crude oil. Instead, Zimbabwe behaves like a country buying close to the spot price and living hand to mouth. That is why it is so often first to adjust. Not because it is uniquely honest, efficient or clairvoyant, but because it has less room to pretend.

The SADC comparables also expose the ZiG problem. Elsewhere, foreign currency markets are allowed at least some freedom to breathe. As geopolitical events buffet commodity markets, currencies like the rand and the kwacha strengthen and weaken in response. It is part of the shock absorber.

When gold and platinum prices rose, South Africa, being mineral rich, saw the rand strengthen. When oil rose, the rand weakened. For consumers paid in rand, the pain is delayed and partly spread out. The same is true of the Zambian kwacha when copper prices surge. It can strengthen on the way up, then weaken and absorb part of the import cost on the way down.

In Zimbabwe, by contrast, the ZiG sits there like a portrait on the wall, unmoved by events, while the central bank insists it is backed by gold. Other currencies in the region are pure fiat and yet somehow manage to behave more honestly.

What does this mean for Zimbabwe? I often run polls and questionnaires on X (Twitter) to gauge sentiment. As gold prices rose, I asked whether people would hedge. Most said no. They wanted to ride the wave.

Zimbabweans are natural risk-takers and that national habit seems to have travelled all the way into government. But the whole point of derivative markets is to hedge, not merely to cheer from the sidelines while prices soar. Reserves, too, are meant to do a job. They are supposed to cover six months or more and act as a hedge against volatility. So if gold is rising, hedge. There is nothing foolish about hedging at $3,800 an ounce if it gives you cover on the cost side as well.

The ban on mineral ore exports may prove one of the more self-defeating policy choices of the period. Australia, under a liberal social democratic government no less, had the sense to let ore exports to China surge and ended up as one of the few countries posting a budget surplus.

South Africa, meanwhile, has idle smelters because many are loss-making. the government of Zimbabwe looked at this landscape and somehow picked the worst of both worlds, the wrong policy at precisely the wrong moment.

Meanwhile, production and supply chains in Zimbabwe almost entirely depend on road because rail is defunct. Yet if ever there was a sector that could have underwritten rail revival, it was mining. The miners would have been the biggest beneficiaries, especially on export corridors into China-linked trade routes. The government did not need to do everything itself. It merely needed to provide the right framework and stick to it long enough for private capital to believe it.

Markets are better at solving these issues – free markets in the foreign currency, fuel and mining sectors – and not government directives.

Tinashe Murapata is a Zimbabwean economist and podcaster